Welcome to our October newsletter, where we’ll explore residential real estate trends in San Francisco and across the nation. This month, we examine the state of the U.S. housing market now that much-needed supply has come to the market. We also explore why the worker shortage may not be as detrimental to the economy as was originally expected because of the renewed growth of entrepreneurship.

With the increase in supply, we’ll probably see the beginning of some market cooling — but in the context of the hottest housing market in history. Housing inventory in the United States continued to rise in August, up 30% from the record low in April 2021. We’re happy to see more homes on the market because they will help satiate the high buyer demand. Although this increase in housing inventory is meaningful, there are still 74% fewer homes on the market than a year ago. The housing market will likely start to see some price corrections as it returns to a steadier state of growth.

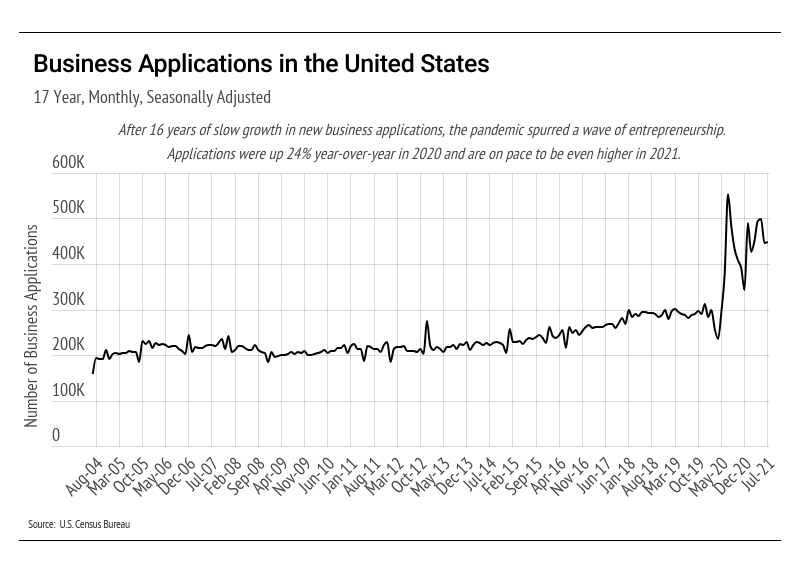

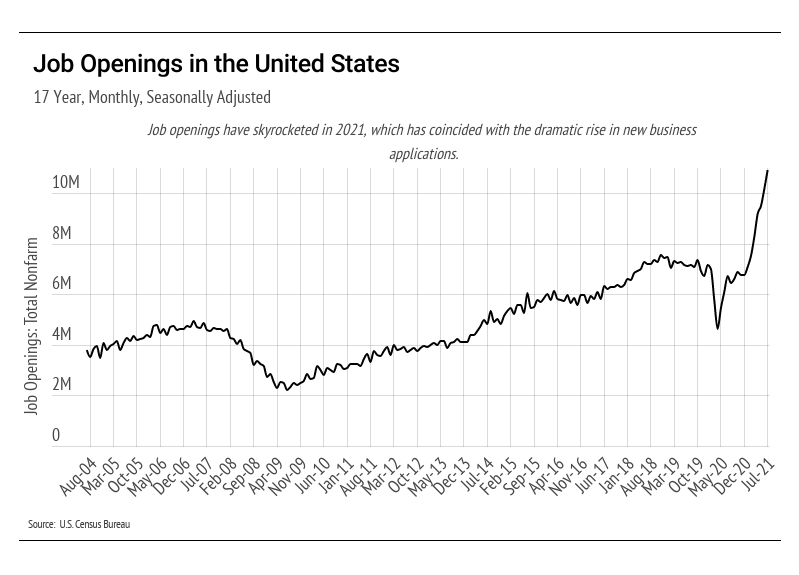

While we, at first, worried that the worker shortage could hurt the economy, it looks like the rise in entrepreneurship is helping to boost production and improve the economy. We often look at jobs to gauge the health of the economy: more employed workers usually means more production and more wealth, which, in turn, means appreciating asset prices. For many months, unemployment stood at around 10 million workers; however, we have started to meaningfully close the unemployment gap, and unemployment has been reduced to 8 million workers. As risks from the delta variant wane, we’ll likely see more unemployed workers reentering the workforce.

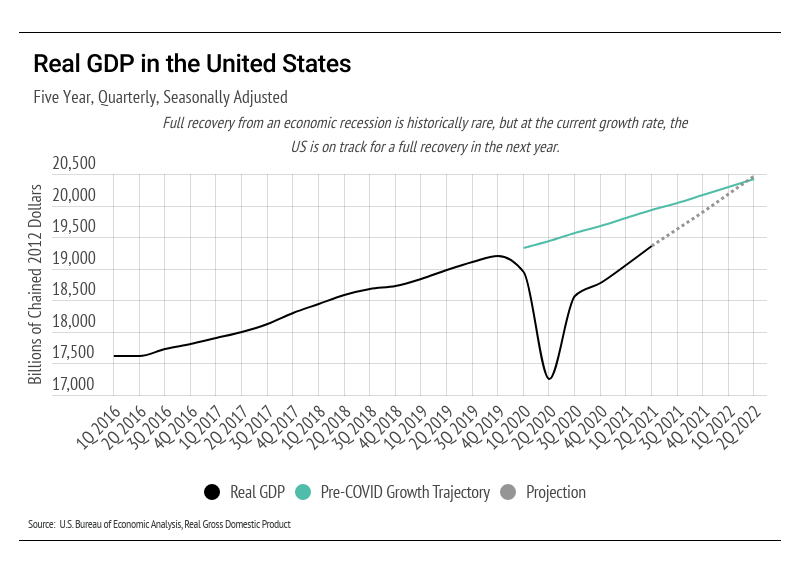

Despite the high rate of unemployment and record number of job openings, U.S. production is climbing rapidly. In terms of GDP, which is the broadest measure of goods and services produced, our economic recovery could reach where we would likely be if the pandemic had never happened within the next year. It cannot be overstated how rare it would be to return to pre-recession GDP, but we might just get there. A potential factor in the rise of both production and job openings is the resurgence of entrepreneurship, which is often associated with higher production.

We remain committed to providing you with the most current market information so you feel supported and informed in your buying and selling decisions. In order to better explore how the above national trends in the economy and housing market are affecting San Francisco, this month’s newsletter will cover the following: - Key Topics and Trends in October: Current trends in the labor force will have long-term effects on the housing market and overall economy.

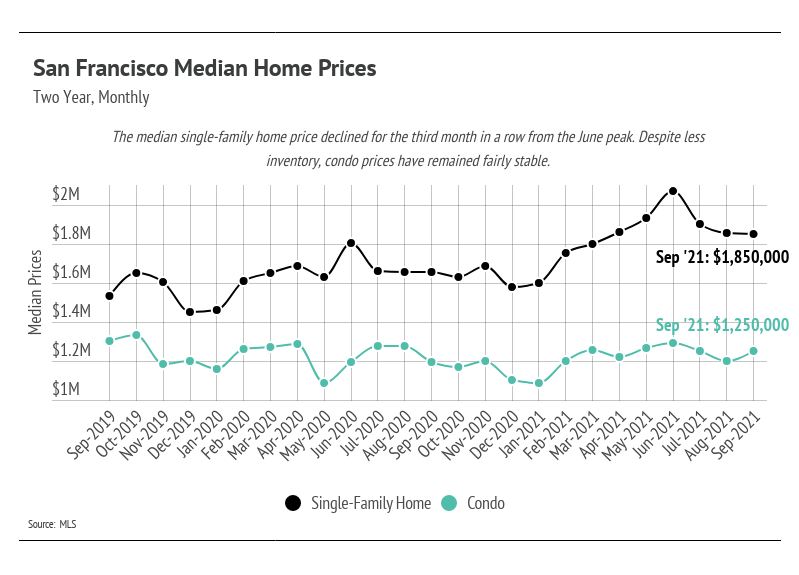

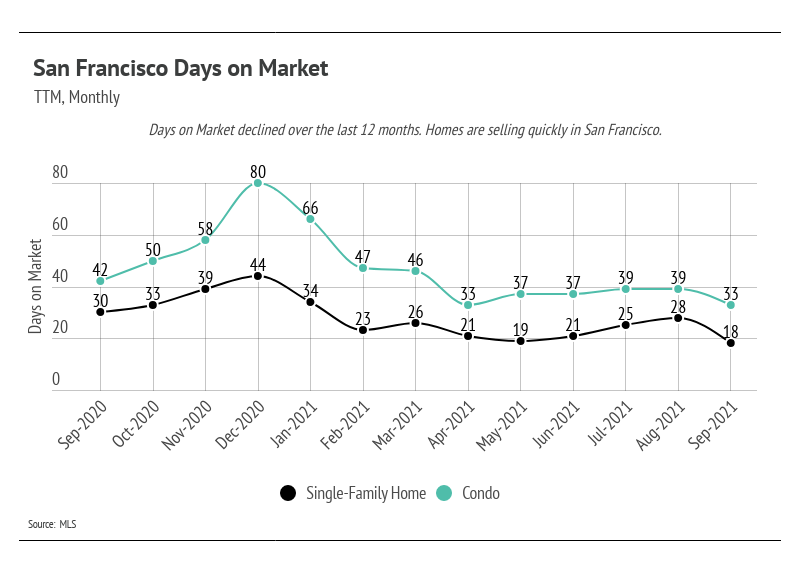

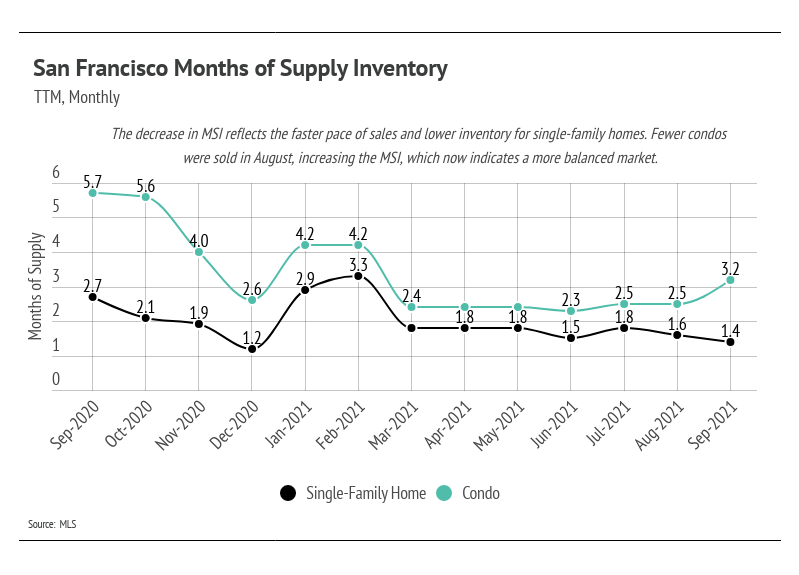

- October Housing Market Updates for San Francisco: Single-family home prices fell, while condo prices rose. The rapid price appreciation we’ve seen over the last year for single-family homes has decelerated.

|