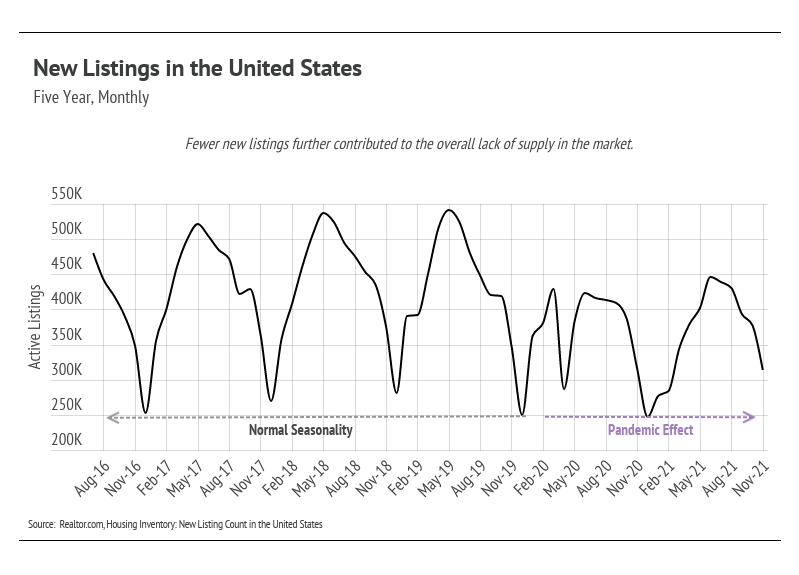

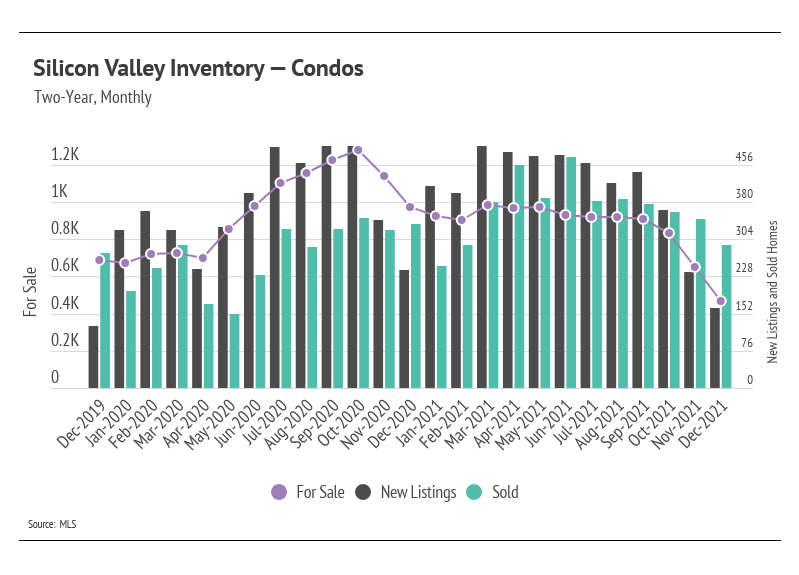

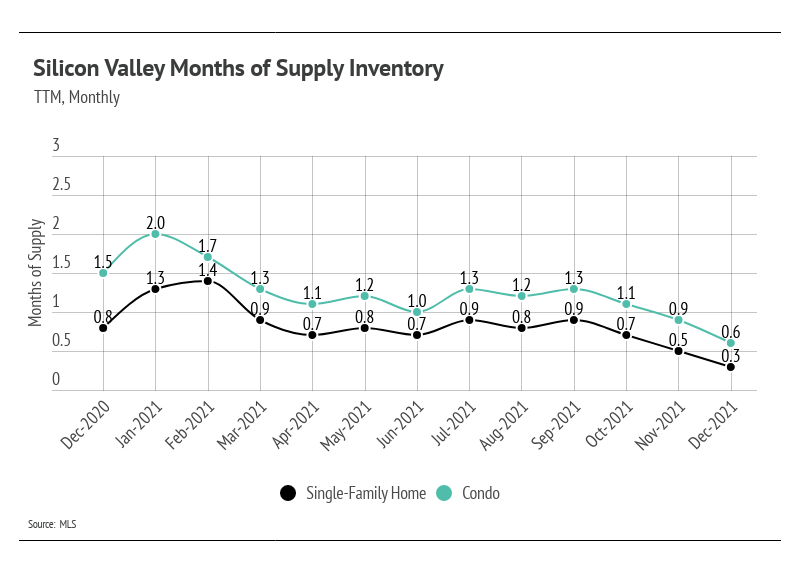

The driving force behind the substantial price increases over the past two years has been the supply of homes, or lack thereof. So, will the housing shortage reverse? The answer is no, as there is no reasonable scenario that would bring active listings to pre-pandemic norms. Before February 2020, seasonal inventory typically peaked in the summer months, but it was trending slightly lower each year. In 2016, inventory peaked at 1.55 million active listings, and by 2019, the peak fell to 1.35 million homes. Inventory in 2021 reached its highest point at approximately 621,000, a 54% decline over two years. Homebuilders simply cannot build fast enough, especially in sought-after urban areas that have already been developed, and new listings are peaking far lower than the historical seasonal norms.

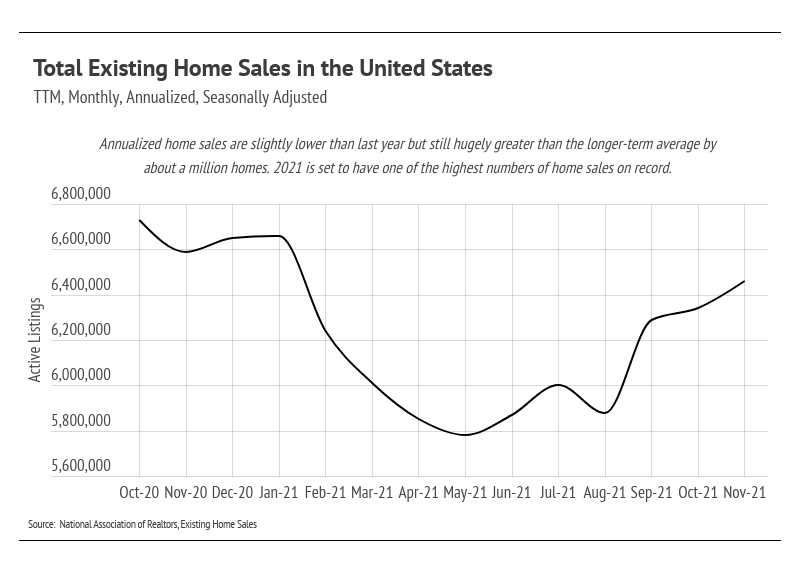

At the same time, we are on pace to see around a million more homes sold in 2021 than in a typical year, based on the long-term average. In other words, more homes are selling, despite the historically low inventory, which is further driving down inventory. In 2022, we expect demand to remain elevated and supply depressed, which should keep home prices from depreciating.

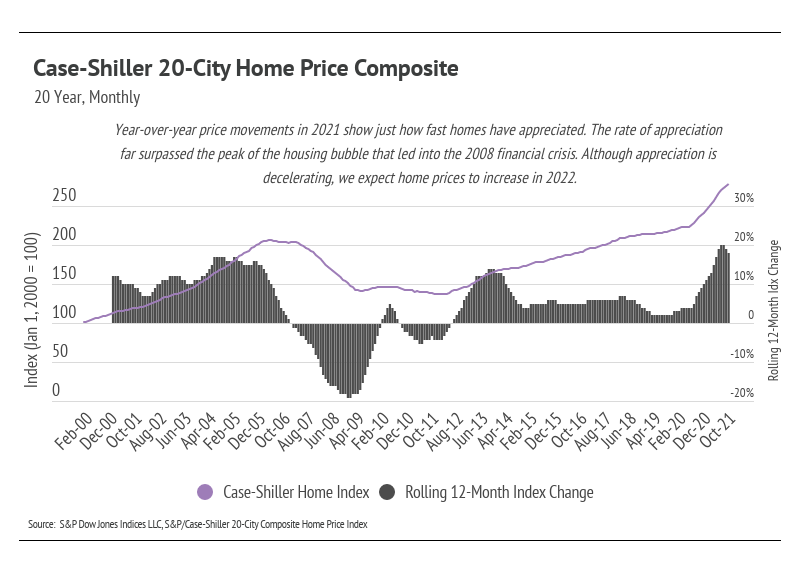

Price appreciation likely will not see the record gains we experienced over the past two years, which is actually good. If we learned one thing from the mid-2000s, we know that we don’t want another housing bubble. The deceleration in price increases, therefore, actually benefits the current market. From a practical standpoint, home prices rising at 20% per year is unsustainable and would certainly cause a major collapse. Moving through 2022, we expect year-over-year price increases to move back to historical norms, in the 5–10% range.

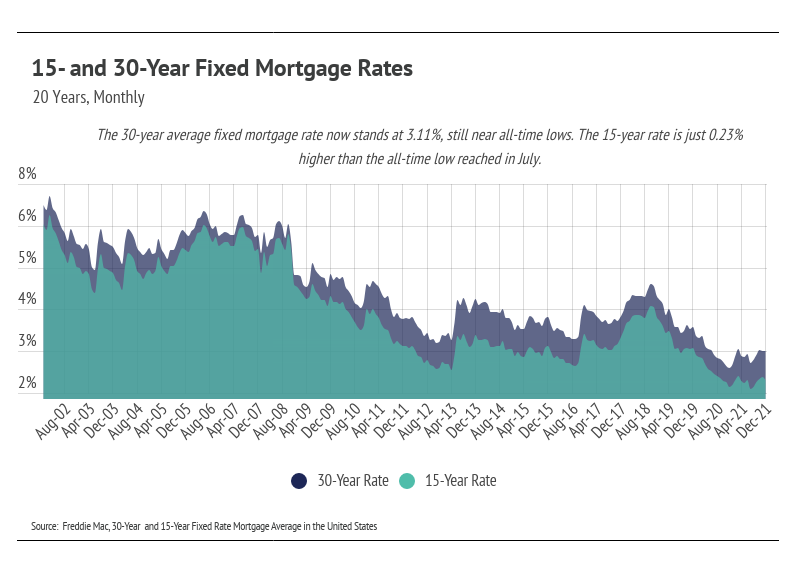

Fed rate hikes in 2022 could drastically affect appreciation as well, which, again, isn’t a bad thing. The low-cost financing we’ve seen over the past two years could be coming to an end (although it’s difficult not to take a believe-it-when-I-see-it-approach to rate increases). When we account for current inflation, which is the highest it’s been since 1981, the real rate of borrowing is negative if you borrow at a rate below 6.8%. Simply put, you’re getting paid to borrow! We don’t expect this phenomenon to last long — it’s a fairly unique situation.

The market remains competitive for buyers, but conditions are making it an exceptional time for homeowners to sell. Low inventory means sellers will receive multiple offers with fewer concessions. Because sellers are often selling one home and buying another, it’s essential that sellers work with the right agent to ensure the transition goes smoothly. |

|