Seasonality in the housing market was incredibly steady before the pandemic. Prices typically rose from January to June, when inventory was low but rising, and then flattened from July to December, when inventory was high but declining. In January 2020, homes were already undersupplied, hitting a record low with just over a million homes for sale on the market. When the pandemic hit, demand for homes exploded, dropping inventory to shockingly low levels. During the 18 months between January 2020 and June 2021, inventory declined 49% and prices increased 32%, doubling the total price increase of the previous three years combined. By January 2022, inventory had reached an all-time low, down 60% in the past two years, while home prices reached a record high, up 34%.

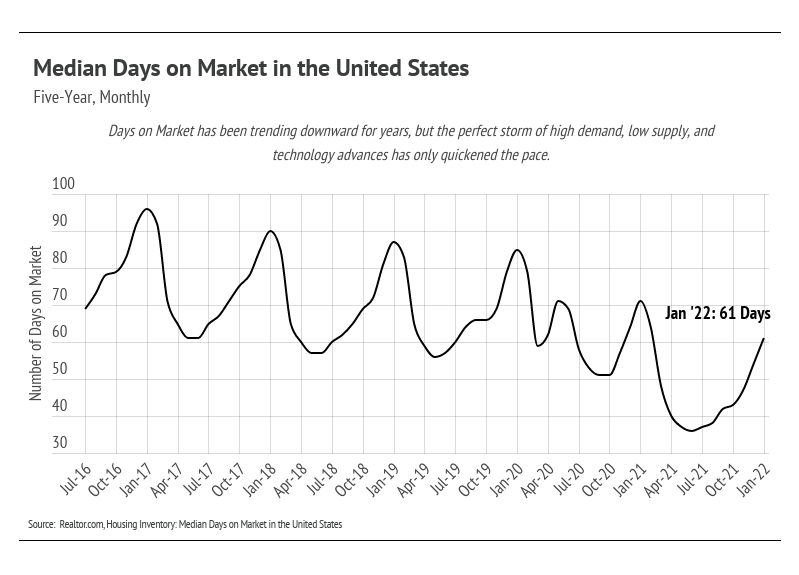

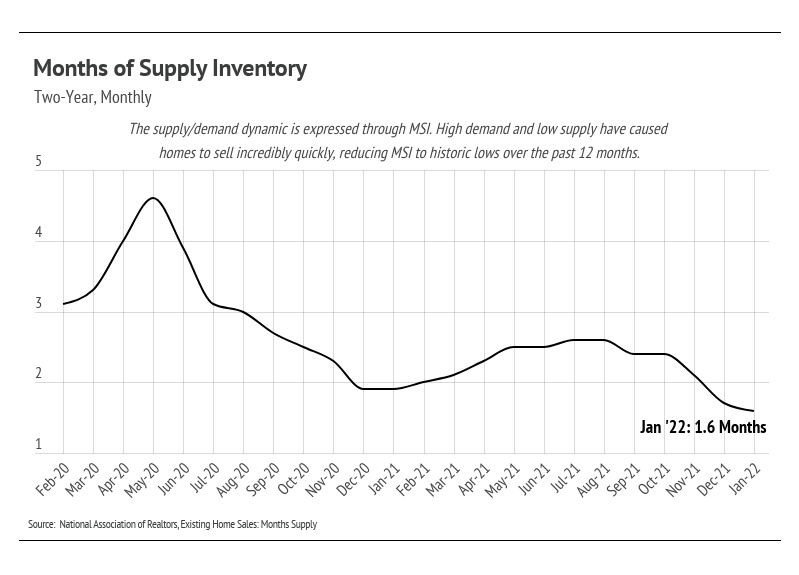

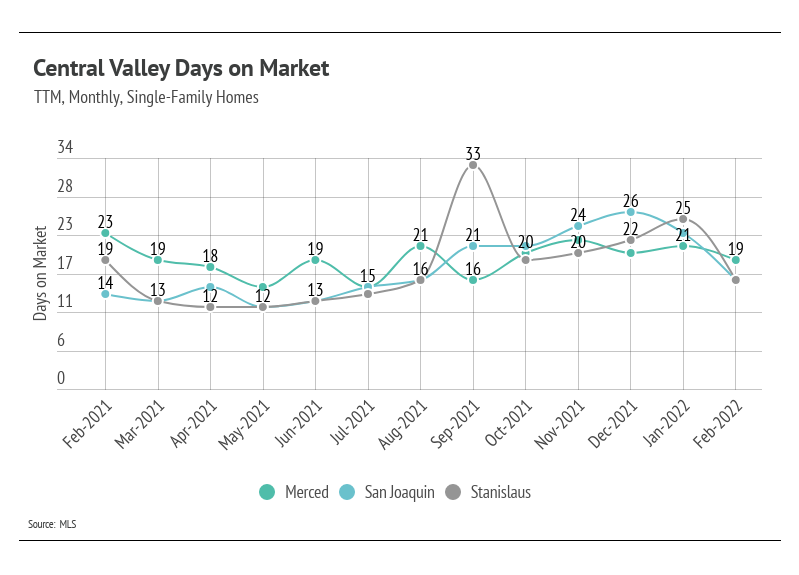

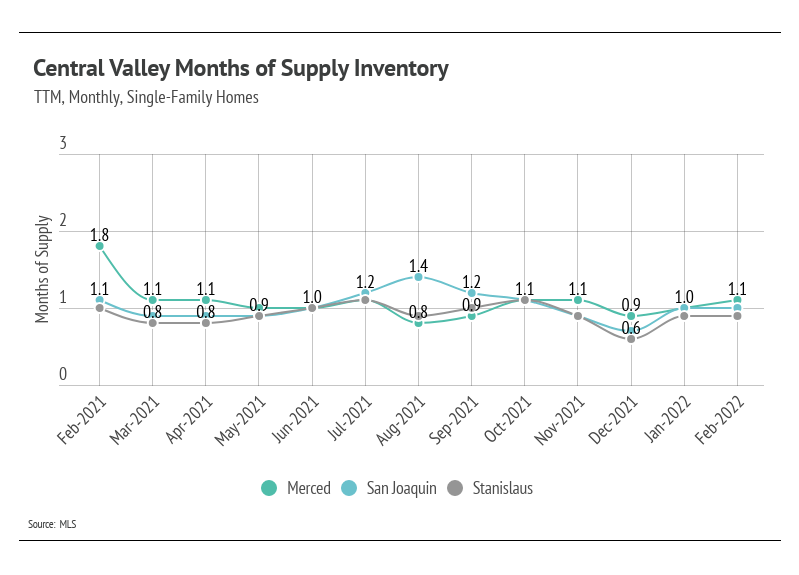

Home sales have only gotten quicker as the market has become more efficient. We can see this trend through the Days on Market and Months of Supply Inventory (MSI). Before the pandemic, homes were already selling more quickly, primarily because of technology and an increasingly competitive market. A more efficient market matches the right people with the right home at a fast pace, causing a drop in supply when new homes aren’t being built. MSI, which quantifies the supply-and-demand relationship, is at a record low, further indicating a sellers’ market. The low supply, high prices, and speed of purchases have shifted homebuyer makeup.

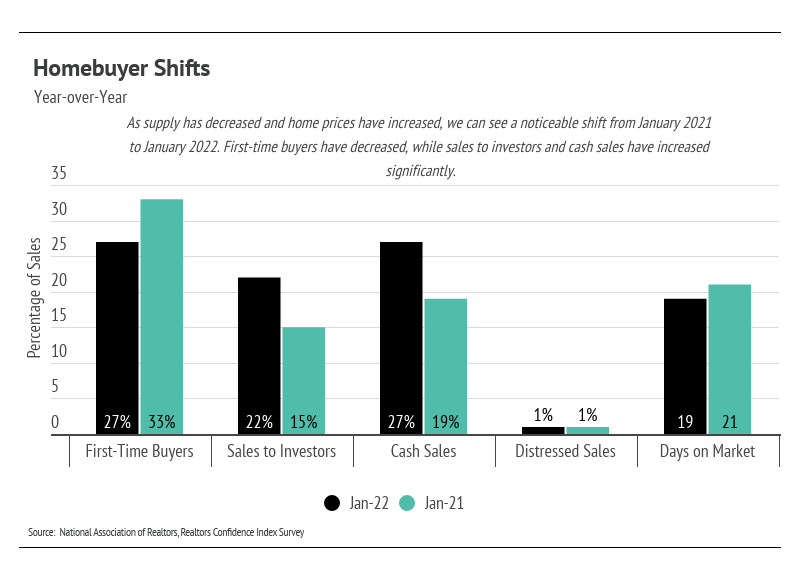

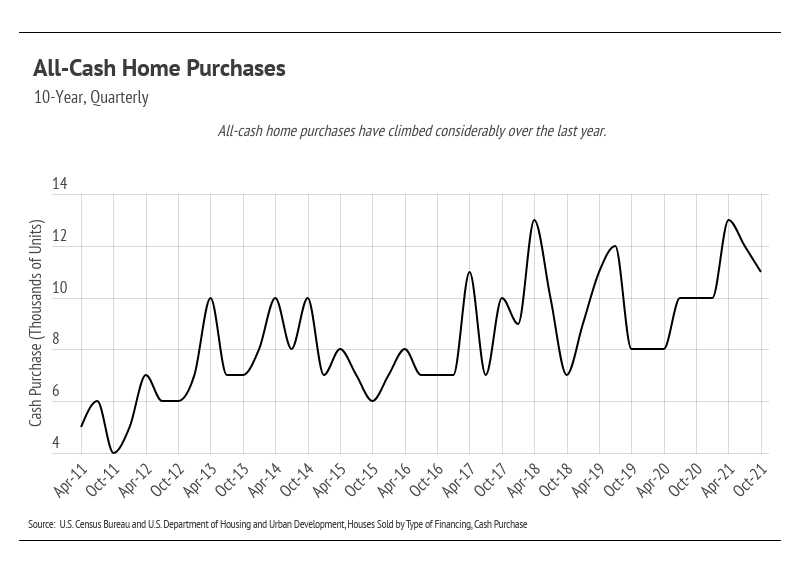

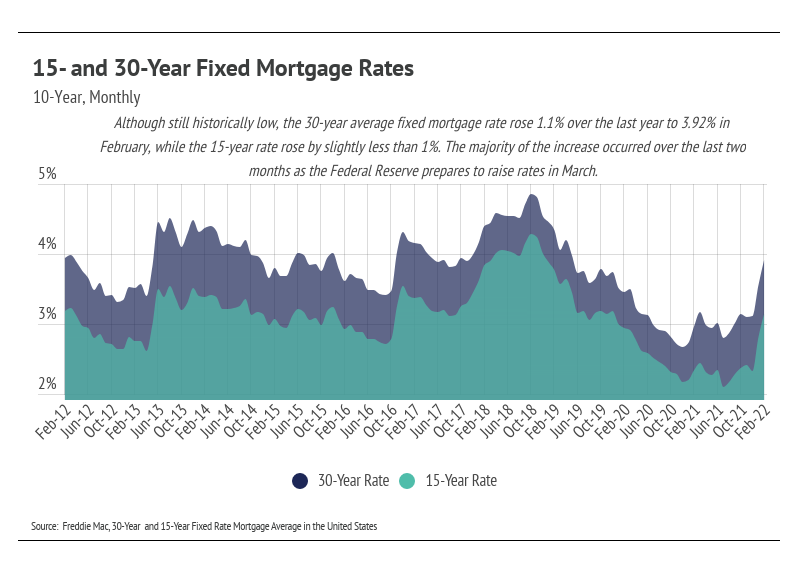

The number of first-time buyers dropped 6% over the past year, while sales to investors rose 7%. All-cash offers increased significantly, often disproportionately affecting first-time buyers, who are most likely to need financing. With rising mortgage rates, many first-time buyers will once again be hit hardest with higher monthly payments. Rates have already risen, because the Fed is expected to start increasing rates in mid-March, and they will only climb higher. Because of the rising cost, the average age of homebuyers is climbing. The average first-time buyer is now 33 years old, and the average repeat buyer is 56 years old, an all-time high. As we enter a new chapter in the housing market, one characterized by rising rates and very low supply, demand can only go one direction: down. But for now, prices aren’t in danger of declining.

Over the next several months, we expect supply to matter more than the interest rate hikes when it comes to home prices. Economists anticipate that the Fed will start the first of six incremental 0.25% increases in March. The Fed uses interest rates in particular as a tool to meet its dual mandate of maximum employment and price stability. With inflation at a near-40-year high, prices for most goods are rising while incomes are not. This situation gives the Fed little choice but to raise interest rates. Essentially, when the cost to borrow increases, fewer people want to borrow, leading to less consumer spending (less demand), which lowers prices.

As we enter this new chapter of rising mortgage rates, we don’t expect home prices to decline significantly, if at all, because supply is still such a driving factor. The low supply means that demand can decline without negatively impacting prices. We don’t expect home prices to appreciate at the record level we experienced over the past two years, but we do expect to see an increase. We are still in the middle of one of the strongest sellers’ markets in history. Buyers must come in with fast, competitive offers in this environment. |

|